The Retirement Rise 1.30.2023

The Retirement Rise 1.30.2023

No Jobs Recession Here; Is the 60/40 dead?; 3 Words to Minimize Regret

This Week’s Good Financial News

Despite all the hemming and hawing in the news media, the job market remains strong.

For example, seasonally adjusted initial unemployment claims were 186,000 last week, 6,000 below the previous week’s number. This was below most economists’ estimates.

An Investment Note for Retirees

2022 was one of the worst years ever for the commonly used 60/40 portfolio, and it was certainly the worst since 2008. The 60/40 portfolio is shorthand for an allocation of 60% stocks and 40% bonds. Stocks offer growth, while bonds usually offer income and protection against stock market volatility. Many investors enjoy its moderate, middle-of-the-road feel.

Unfortunately, last year was uniquely bad for the 60/40 portfolio due to extremely low starting interest rates and surging inflation.

From Morningstar:

There’s no doubt about it: Last year was a disaster for investors relying on bonds to protect against a significant drop in the stock market.

On the stock side of the equation, the Morningstar US Market Index fell 19.4% in 2022 for its biggest loss since 2008. Meanwhile, the Morningstar US Core Bond Index had the worst year in its history, down 12.9%.

Put the two together and it was bad news for investors. The Morningstar US Moderate Target Allocation Index—a diversified mix of 60% equities and 40% bonds designed as a benchmark for a 60/40 allocation portfolio—fell 15.3% in 2022, just 4 percentage points better than the stock market’s decline of 19.4%, as measured by the Morningstar US Market Index. Those double-digit losses made for the 60/40 index’s worst calendar year since 2008.

So what now? Is diversification dead?

No. Diversification still matters, and we have consistently argued for global diversification in your stock portfolio. An appropriate amount of diversification between stocks and bonds, based on your age, risk capacity, and goals, is also important.

Bonds offer a degree of security for near-term cash flows (1-5 years or 1-7 years). Stocks offer

Dimensional had the following to say:

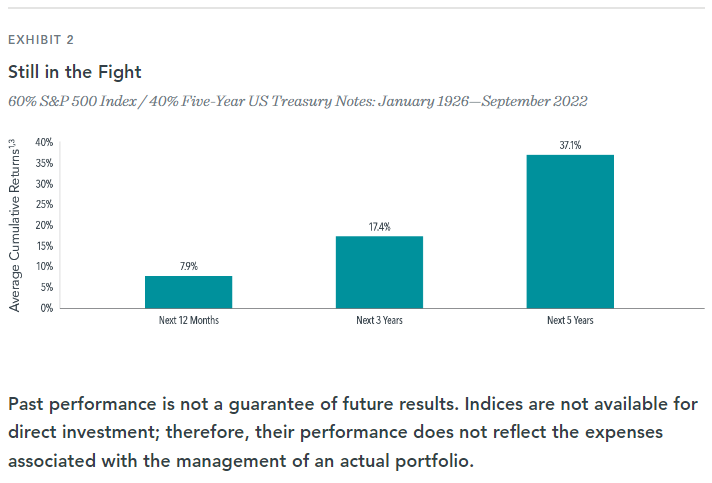

It is important, and especially so during difficult market conditions, for investors to focus not solely on where returns have been but also on where they could be going in the months and years ahead. Looking at the performance of a 60/40 portfolio following a decline of 10% or more since 1926 (see Exhibit 2), we see clearly that returns on average have been strong in the subsequent one-, three-, and five-year periods. History makes a strong case for investors to stick with their longer-term plan and should help serve as a reminder that steep declines shouldn’t derail investors’ progress toward reaping the expected benefits of investing.

A Thought on Retire on Purpose

In his latest book, The Power of Regret, author Daniel Pink summarized nearly 15,000 regrets from individuals across 100 countries. His biggest takeaway?

Always Reach Out.

According to Inc.com:

"What really stuck with me were the stories about people in relationships that had drifted apart who didn't reach out. And then in some cases it was too late, and in other cases, it was just bugging them the whole time," Pink reports.

The stubbornness with which people fail to heal fraying relationships frustrated Pink. At least until he realized that he too was guilty of failing to reach out to people he knew he should reconnect with. "I thought of the proverb 'Physician, heal thyself,'" he says. "I realized, Wow, I don't take my own advice on that. And for the exact same reason. Those stories changed both my perspective and my behavior."

The experience has left Pink with a new three-word rule for reducing his own regrets. "Now my own mode as a human being is that if I'm at a juncture where I'm saying, 'Should I reach out or should I not reach out?' I know the answer," he says: "Always reach out."