The Retirement Rise 3.6.2023

The Retirement Rise 3.6.2023

On Innovation, Investing for Decades, and

If you don’t design your own life plan, chances are you’ll fall into someone else’s plan. And guess what they have planned for you? Not much. - Jim Rohn

This Week’s Good Financial News

Often, innovation and technological advancement are framed as bad for workers. Over the short term, this can be true. For example, no one wanted to be a stagecoach manufacturer when Ford started kicking out Model-Ts. But ultimately, innovation has created opportunities for millions of workers. For example, coding didn’t exist in the 1950s. Now, estimates suggest there are about 27 million software engineers globally.

However, this can apply to more traditional industries as well. For example, according to The Wall Street Journal, we will need many more electricians as America tries to electrify.

From the article:

The current total of more than 700,000 electricians in the U.S. is expected to grow about 7% over the next decade, slightly faster than the nationwide average of 5%, according to the Bureau of Labor Statistics. The shift to renewable energy and the need to update electrical systems is expected to drive that growth. Some analysts say that expansion needs to be several times faster for the U.S. to meet its climate and electrification goals.

The BLS includes a separate category of solar photovoltaic installers, some of whom could also be electricians. Growth in that much smaller sector is expected to be above 25%.

Over the short term, this might add to inflationary pressures as there is a shortage of electricians. But ultimately, a signal is being sent that we need more electricians to do this exciting work, like electrifying and decarbonizing the power grid, which pays great.

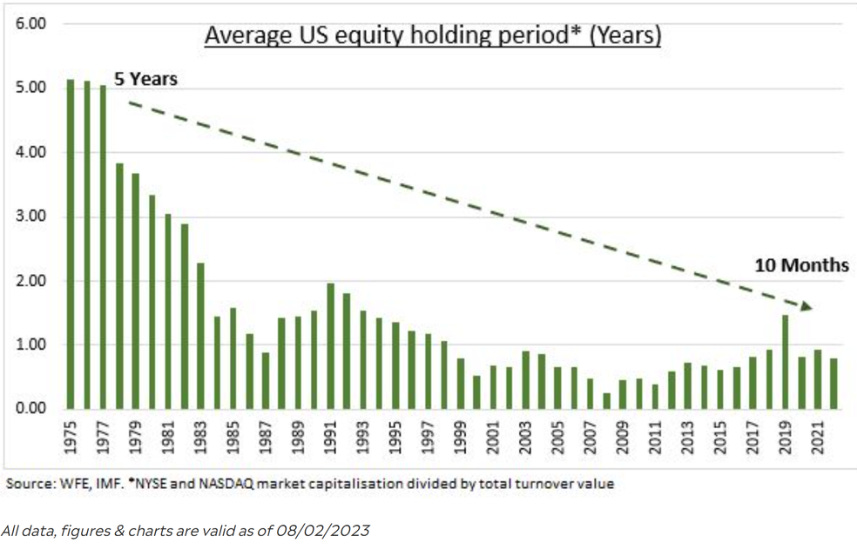

An Investment Note for Retirees

The ‘I’ in the Retirement RISE stands for ‘Invest for a Better Future.’ Implicit in this is the idea that you may have to invest for years or even decades before the intended future arrives. So, for example, a 20 or 30-year-old who is investing for retirement will hopefully allow their investments to compound for over 30-40 years.

Similarly, a 65-year-old retiree must invest for cash flow the following year just as much as for income when they are 95. That’s still a 30-year time horizon! And, of course, that demands a 30-year investment strategy, like a diversified portfolio of global stocks.

So, imagine my dismay reading that the average investor holds stocks for less than a year. In 2022, that number was ten months!

The most important part of your investment plan is the ability to stick with it. Unfortunately, most investors haven’t received the memo.

A Thought on Retire on Purpose

In the book Broadcasting Happiness, author Michelle Gielan tells the story of a couple concerned about their retirement. Given current spending and rates of return, the husband was stressed because he felt they would run out of money in their 80s.

The wife, an optimistic and skilled thinker, started wondering what items his analysis was extrapolating into the future they didn’t need. Her answer? The house!

“Honey,” she says (and I’m paraphrasing), “You are assuming we stay in our current house indefinitely. What would happen if we moved to the Southwest where houses and the cost of living are lower?”

It turns out that between the lower monthly expenses in the Southwest and the extra cash from their potential house sale, their retirement looked much more sustainable.

So here’s the question: What belief or supposition are you extrapolating into the future that is causing stress that could be considered differently in a way that results in more optimism and pragmatic positivity?

So often, prospective retirees and retirees don’t need more money. Instead, they require less of whatever they don’t need.